We are more in the midst of a continuation of the erratic phase that began with the pandemic. Uncertainties are mounting: geopolitical, trade-related, climate-related, and political. Donald Trump’s return is amplifying certain tensions, but they would not disappear without him.

Global trade has become a central issue. China is steadily gaining market share, particularly in Europe, prompting the European Commission to consider or implement trade defense measures. This trend is set to continue.

Aggregate growth figures are becoming harder to interpret. In the United States, for example, the gap between the richest 10% and the poorest 30% continues to widen. The S&P may be near its all-time highs, yet consumer confidence remains very low.

Added to this is climate risk, which I consider one of the most underestimated risks. Climate volatility is itself becoming a source of economic uncertainty.

Overall, information circulates faster, capital moves faster: shocks are therefore more frequent, even if their magnitude may vary.

The Chinese economy is highly segmented today. On the one hand, exports are still performing very well. China is producing on a massive scale, building up inventories, and directing them toward export. This is what sustained its model in 2025. But this momentum is running out of steam as global trade slows.

The composition of Chinese exports is also changing profoundly: about 30% now fall under the high-tech category. Beijing wants to shift its economy from the old world to the new, with the goal of having high-tech quickly account for more than 20% of GDP.

The problem is domestic. Consumption is slowing, retail sales have posted one of their worst performances since the Covid period, and certain service indicators, such as domestic air traffic, are deteriorating. Real estate remains a major drag: prices are falling less than before, but they continue to decline, while 60 to 70% of Chinese household wealth is invested in property. This creates a negative wealth effect.

China is therefore expected to reintroduce new support measures, particularly for consumption, real estate, and the technology sectors. Climate risks could also weigh heavily on economic activity this summer, particularly due to floods or extreme weather events.

For Europe, the impact is doubly negative: it is exporting less to China because domestic Chinese demand is weak, and at the same time it faces Chinese competition in growth sectors. The example of hybrid cars is telling: Chinese manufacturers are projected to have grown from about 3% market share in Europe at the end of 2024 to nearly 20% based on the latest data cited. The Europe-China trade deficit in goods is therefore set to continue widening.

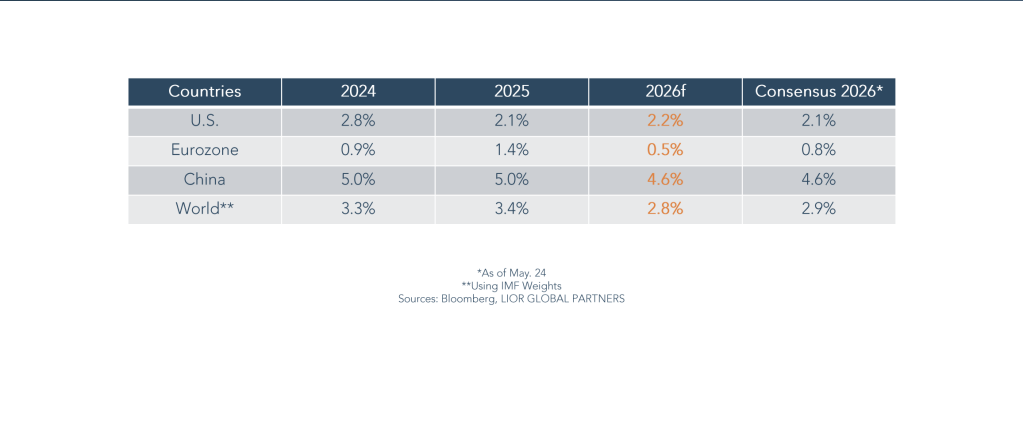

For 2026, several factors continue to support the U.S. economy. We are forecasting a slight acceleration, to around 2.2% compared to 2.1% last year.

First, there are tax cuts and tax refunds, which supported consumption in March and April. Next, the wealth effect: the top 10% of households reportedly hold about 87% of stocks and funds, and continue to spend when markets are high. They now account for nearly 50% of total consumption.

The third driver: massive investments in artificial intelligence. CAPEX projects are underway and are contributing positively to growth. The fourth factor: productivity, which is improving significantly.

In the short term, the World Cup should also have a positive impact. Additionally, the Supreme Court’s review of certain tariffs could restore some purchasing power to households or provide some breathing room for businesses.

But this growth is highly concentrated. The wealthiest are faring very well, while more vulnerable households are suffering from rising defaults on credit cards and student loans. The housing market remains in recession and has contributed negatively to GDP for several consecutive quarters.

Political risk is also significant with the midterm elections. A loss of the House of Representatives by Donald Trump would drastically alter the political landscape and could usher in a period of instability.

Finally, artificial intelligence is already raising questions about financial sustainability. The most advanced models are extremely expensive. We will need to monitor the actual return on investment, electricity and water requirements for data centers, and environmental constraints. These costs are not always factored into current market expectations.

Sources :

Yes. The main risk is that of a “super El Niño.” El Niño is a natural phenomenon, but its average intensity has been increasing for several years. Current data show highly unusual temperature deviations: in some areas, records are not just being broken, but exceeded by several degrees.

This creates a massive amount of energy capable of triggering significant climate disruptions. The first effects could begin in Asia this summer, continue in Latin America, and then affect the United States during hurricane season.

The exact scale remains difficult to predict, but the risk is widely underestimated by markets, insurers, and economic actors. Issues related to water, fires, natural disasters, and agricultural commodities could become much more central.

Europe is in a very unfavorable position. It is exposed to rising energy prices, particularly for heating oil and imported goods, even though some countries like Italy, Germany, and Spain have taken fiscal measures to cushion the blow.

The sector performing best remains hospitality: tourism, transportation, and restaurants. But it faces capacity and logistics issues. Flights have been canceled or rescheduled, some jet fuel stocks are limited, and this is already weighing on transportation and deliveries.

European households are also more exposed to energy and food costs in their consumer spending. Real purchasing power is therefore more severely affected.

Politically, France, Italy, Germany, and Spain—each major country has its vulnerabilities. Exports are not a sufficient buffer, especially in a context where Europe is caught in a vise between the United States and China.

Germany was set to benefit from a major stimulus in defense and infrastructure, but implementation is slow. The expected effects may materialize later than anticipated. This is one of the reasons why our growth forecasts for Europe are pessimistic, at around 0.5% for the year.

Some countries are faring better—Spain, Portugal, Greece—notably because they remain more affordable and benefit from stronger real estate markets. But the two major engines, France and Germany, are no longer fully fulfilling their role as growth drivers.

First, we need to track artificial intelligence, not only through U.S. markets but also via global token consumption: where it’s happening, which models dominate, and which applications are gaining traction. Rankings are changing very quickly.

Next, we need to monitor global temperatures, as they can have major sector-specific effects starting this summer and into the fall.

The price of heating oil in Europe is also critical, as it can impact inflation, industry, and the entire economic fabric.

We must also monitor fertilizers and agricultural commodities—rice, wheat, and other staples—as they react quickly to weather events and sometimes provide a very concrete reading of the risk anticipated by the markets.

Finally, we must monitor the likelihood of a permanent ceasefire in conflict zones, as well as the political implications of the U.S. midterm elections, particularly the possibility that Democrats will retake the House of Representatives and the Senate.

Yes. To end on a positive note, Monaco enjoys a rare positioning. In an uncertain European and international environment, there are few places that offer security, legal stability, political stability, quality of life, and fiscal predictability all at once.

This is a major draw for capital, talent, and families seeking a stable base. Monaco must preserve its fundamental pillars. In the current context, this relative advantage becomes even more apparent.